.png)

Latin America's financial institutions have invested heavily in fraud prevention over the past three years. They've built behavioral biometrics programs, stood up interbank intelligence-sharing networks, and hardened their transaction monitoring pipelines. None of that matters much when fraudsters skip the transaction layer entirely and compromise the identity at onboarding.

The region's fraud investments were largely shaped by the threats that caused visible losses: account takeover attacks, social engineering scams, RAT-based fund theft. Mexico recorded a 324% increase in account takeover cases between end-2024 and early 2026 (BioCatch). Scam attempts across 36 Latin American financial institutions rose 155% in 2025 alone. Malware attacks increased 225%. These were the threats demanding attention, and attention is what they got.

But while LATAM banks were building defenses for those known attack patterns, a different category of fraud was accelerating in the background. Deepfake-based identity fraud, particularly at the digital onboarding stage, has moved from theoretical concern to operational reality. Most regional fraud teams have not caught up. The detection gap is widening, not narrowing.

- LATAM banks invested in fraud tools designed for account takeover and social engineering, tools that assume the onboarded identity is real. Deepfake fraud breaks that assumption at the source.

- In Q4 2025, 55+ synthetic media generators were released, roughly one every 1.6 days, with 868,000 fine-tuned variants created monthly, many optimized to bypass biometric onboarding (DuckDuckGoose Threat Intelligence).

- Brazil recorded R$10.1 billion in banking fraud losses in 2024, with Pix real-time rails compressing fraud execution to minutes, eliminating the window where post-hoc monitoring can intervene.

- 95% of synthetic identities go undetected during onboarding at financial institutions, according to a Thomson Reuters analysis cited by Themis.

- FATF's December 2025 Horizon Scan classified deepfake bypasses of digital KYC as failures of Customer Due Diligence obligations, creating regulatory exposure beyond fraud losses.

- The cost of synthetic identity creation has dropped to approximately $15 per identity, with generation taking under 30 minutes, bringing fraud-at-scale economics within reach of organized crime networks.

The Investments That Missed the Point

LATAM banking fraud prevention has improved significantly. Argentina's Galicia, Naranja X, and Santander launched BioCatch Trust Argentina in May 2025, the first real-time interbank behavioral fraud intelligence network in the hemisphere, and recorded a 27% decline in mule accounts. Brazil's Central Bank has pushed increasingly sophisticated mechanisms for real-time payment fraud recovery. Across the region, machine learning-based anomaly detection, device fingerprinting, and behavioral biometrics have become standard parts of the fraud stack.

These tools share a common assumption: that the identity on the account is real, and the question is whether the person accessing it is the actual account holder. Behavioral biometrics detects behavioral anomalies in existing sessions. Transaction monitoring flags unusual movement of funds from established accounts. Interbank signals track receiving account activity.

Deepfake fraud inverts this assumption. It doesn't compromise a legitimate account after the fact. It creates a fraudulent identity that passes verification in the first place, establishing an account that looks entirely legitimate from day one. No transaction anomaly. No behavioral deviation. No mule account signal. Just a synthetic person who completed onboarding successfully.

What the Region's Onboarding Infrastructure Was Not Built For

LATAM's digital banking growth has been exceptional. Brazil's Pix payment system drove rapid onboarding at scale across traditional banks and neobanks. Mexico's fintech regulation mandated digital-first processes. Colombia enabled fully digital onboarding with widespread biometric verification. The result is a region where remote identity verification handles enormous transaction volume, but where the underlying infrastructure was designed for an earlier threat environment.

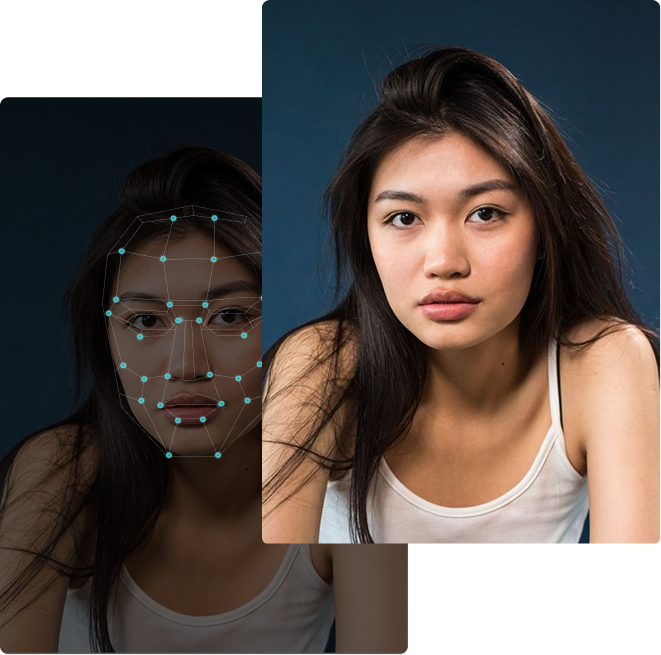

Most digital onboarding systems in the region rely on document verification paired with liveness detection. That combination was robust against early fraud patterns, including photo replay attacks and static image substitution. It was not designed for the current generation of synthetic media.

In Q4 2025 alone, more than 55 synthetic media generators were released at a rate of roughly one every 1.6 days (DuckDuckGoose Threat Intelligence). Image-to-video generation capability expanded by over 1,000% since early 2024. Monitoring identified nearly 868,000 fine-tuned synthetic variants created monthly across open AI ecosystems, with many specifically optimized to bypass onboarding and authentication systems. Each new variant introduces identity characteristics that existing detection models have never encountered, creating exposure windows during which verification systems are blind to threats they haven't been trained on.

Standard liveness detection fails against injection attacks, where synthetic video is fed directly into verification APIs, bypassing the camera layer entirely. The World Economic Forum's Cybercrime Atlas, released in January 2026, examined 17 face-swapping tools and eight camera injection tools and found that most were capable of bypassing standard biometric onboarding checks at financial institutions. These are not experimental exploits. They are readily available, and they are being used.

The Specific LATAM Exposure

Brazil illustrates the gap clearly. Financial institutions there recorded R$10.1 billion in banking fraud losses in 2024. Pix-driven real-time payments compress fraud execution timelines toward minutes rather than hours, which means a synthetic identity that passes onboarding can move funds before any post-hoc monitoring system triggers a review. The threat report published by DuckDuckGoose in March 2026 concluded that the primary risk is no longer manipulated media but synthetic presence: AI-generated individuals interacting with verification systems in real time.

Mexico's identity complexity compounds the problem. The country's ID ecosystem spans over 390 different document types, and key national databases (SAT, INE, CURP) are fragmented and inconsistently maintained. Fintechs operating in Mexico rely on a patchwork of third-party vendors and manual review, creating uneven coverage that sophisticated fraud actors can probe for the weakest entry points. A region where 95% of synthetic identities reportedly go undetected during onboarding (Thomson Reuters analysis cited by Themis) is not a region whose verification infrastructure is ready for the current tool environment.

The regulatory picture adds weight to the risk. FATF's December 2025 Horizon Scan explicitly identified deepfakes as a tool capable of bypassing AML controls, Customer Due Diligence systems, and digital identity verification at onboarding, and signaled that supervisors will scrutinize deepfake controls as part of standard AML reviews. A financial institution that accepts a synthetic identity at onboarding doesn't just face a fraud loss. Under current regulatory interpretation, it faces potential exposure for CDD failure.

Why Fraud Teams Haven't Prioritized This

The gap between the threat and the response isn't negligence. It's a measurement problem.

Account takeover fraud produces visible signals: legitimate customers report unauthorized transactions, banks see behavioral anomalies in account sessions, and transaction monitoring systems catch unusual patterns. The loss is attributable and the victim is identifiable. Deepfake onboarding fraud produces none of these signals. The fraudulent identity completes onboarding successfully, the account sits dormant or moves small amounts, and the connection to synthetic identity fraud only becomes visible, if at all, during a forensic review after a larger fraud event.

This asymmetry means deepfake onboarding fraud is systematically undercounted in regional fraud statistics. Teams allocate resources to the fraud that appears in their reporting. Fraud that doesn't trigger existing detection systems doesn't appear in reporting, so it doesn't drive resource allocation. The blind spot is self-reinforcing.

There's also a vendor-side explanation. Most fraud prevention vendors serving the LATAM market built their platforms around the ATO and social engineering threats that drove the last wave of procurement decisions. Behavioral biometrics, transaction monitoring, and device intelligence are well-represented in regional vendor stacks. Deepfake-specific detection, designed to evaluate the authenticity of biometric inputs at onboarding rather than behavioral patterns in existing sessions, is less common. Buying committees haven't consistently asked for it, so fewer vendors have offered it.

What Changes When You Look at the Onboarding Layer

Addressing deepfake risk at onboarding is a different technical problem than addressing fraud in authenticated sessions.

Behavioral biometrics work on the assumption that humans and automated systems interact differently. Deepfake detection works on the assumption that genuine biometric inputs and synthetic ones have different artifact patterns, inconsistencies in pixel distribution, temporal incoherence in video, frequency-domain signatures that differ from live capture. These are specialized detection tasks requiring models trained specifically on the output characteristics of deepfake generation tools.

The detection challenge is genuine: as generator quality improves and new variants proliferate, detection models trained on earlier tool outputs develop blind spots for newer ones. The appropriate response isn't to abandon detection but to treat it as continuously adaptive infrastructure rather than a one-time procurement decision. DeepDetector is designed for exactly this environment, providing real-time explainable analysis of biometric inputs within large-scale onboarding flows, with ongoing model updates as the generator landscape evolves.

Several categories of additional signal can improve onboarding security without requiring a complete system replacement. Device and network context provides pre-verification risk signals: IP characteristics, device fingerprint inconsistencies, virtual camera indicators, and behavioral patterns in the onboarding session itself can flag elevated-risk submissions for additional scrutiny before biometric analysis. Document-biometric consistency checks, comparing the document photograph with the submitted biometric rather than treating each as an independent pass/fail, reduce the attack surface for injection approaches. Layered verification isn't one powerful tool. It's multiple overlapping signals making the fraud task substantially harder.

Where This Is Heading

The cost of deepfake-based identity fraud tooling has dropped to approximately $15 per synthetic identity, with generation taking under 30 minutes. Fraudsters operate with the economics of scale. A fraud organization with access to commodity AI generation tools can test onboarding systems at volume, probe for detection gaps, and iterate faster than most verification vendors push model updates.

LATAM's digital banking growth shows no sign of slowing. Brazil's neobank sector continues to expand. Colombia and Peru are seeing rapid growth in digital-first financial services. Mexico's fintech ecosystem is scaling despite regulatory complexity. Every new account opened remotely is an onboarding event, and the volume of synthetic identity probing will scale with the volume of legitimate onboarding.

Two developments will shape the next 18 months. First, regulatory pressure will increase. FATF's 2025 guidance is a leading indicator, not a final position. As jurisdictions in LATAM develop their own AI-era AML frameworks, deepfake controls at onboarding will move from best practice toward required practice. Institutions that have built the capability ahead of regulatory mandates will face less disruption than those implementing it under compliance pressure. Second, the generator landscape will continue to fragment. The 868,000 fine-tuned variants identified monthly in early 2026 will not decrease. Detection models that can't keep pace with generator evolution will provide diminishing protection, making continuous model adaptation a structural requirement rather than a vendor differentiator.

The institutions that come out of this period well won't be those that responded fastest to account takeover attacks in 2024 and 2025. They'll be the ones that diagnosed the blind spot in their onboarding layer before it produced the kind of visible fraud losses that make the diagnosis obvious.

FAQ

What is deepfake fraud in banking?

Deepfake fraud in banking refers to the use of AI-generated or AI-manipulated biometric content, typically synthetic faces, video, or voice, to impersonate a real or entirely fictional person during identity verification. At onboarding, this allows fraudsters to create accounts under synthetic identities that bypass standard verification controls.

Why are LATAM banks particularly exposed to deepfake onboarding fraud?

LATAM banks have invested heavily in fraud tools designed for account takeover and social engineering attacks, which produce visible transaction-layer signals. Deepfake fraud at onboarding produces no such signals: the synthetic identity passes verification and the fraudulent account looks legitimate from day one. The detection gap reflects the shape of prior investment, not institutional negligence.

What is an injection attack in identity verification?

An injection attack bypasses the camera or biometric capture layer entirely by feeding pre-generated synthetic video directly into a verification API. Rather than holding a deepfake image in front of a camera, the attacker routes AI-generated video through virtual camera software directly to the onboarding system. Standard liveness detection, designed to catch replay attacks, does not catch injection attacks.

How fast is the deepfake tool landscape evolving?

In Q4 2025, more than 55 synthetic media generators were released, roughly one every 1.6 days. Image-to-video generation capability expanded over 1,000% since early 2024. Nearly 868,000 fine-tuned synthetic variants are created monthly across open AI ecosystems. This pace means detection models trained on earlier generator outputs develop blind spots for newer ones within months.

What regulatory risk does deepfake onboarding fraud create for financial institutions?

FATF's December 2025 Horizon Scan classified deepfake bypasses of digital identity verification as failures of Customer Due Diligence obligations, not merely technical security lapses. A financial institution that accepts a synthetic identity at onboarding may face regulatory exposure for CDD failure. FATF has signaled that supervisors will scrutinize deepfake controls as part of standard AML reviews.

.webp)

About the author