Introduction

As deepfakes and synthetic identities reshape the fraud landscape, compliance has become a frontline defense rather than a back-office obligation. Regulators are raising the bar globally, demanding AI-powered systems, layered KYC processes, and continuous monitoring to counter evolving risks. This article breaks down what 2025’s compliance landscape looks like, the new regulatory expectations, and how organizations can stay ahead of enforcement trends.

Key Takeaways

- Regulators are escalating enforcement against AI-enabled fraud, issuing record AML and KYC fines in 2025.

- New frameworks like the EU AI Act, FATF digital identity guidance, and the UK’s “failure to prevent fraud” law redefine compliance obligations.

- Financial institutions are expected to integrate AI-powered monitoring, liveness detection, and explainable AI into their fraud prevention systems.

- Compliance is now a competitive differentiator, those investing in adaptive, transparent detection frameworks gain trust and regulatory resilience.

- DuckDuckGoose AI enables real-time, explainable deepfake detection aligned with emerging compliance requirements.

When “Good Enough” Stopped Being Good Enough

TD Bank believed its controls were adequate. U.S. regulators disagreed—to the tune of $3.09B. Over $670M was laundered through its accounts—not because controls were absent, but because they were built for a world of forged documents and stolen IDs, not one of scalable synthetic identities and deepfaked video verification.

They’re not alone. Liminal (2025) reports 87% of FIs feel unprepared to detect deepfakes; 79% struggle to prevent synthetic identities. The gap between what compliance built and what criminals deploy has never been wider—and regulators have run out of patience.

The Numbers Tell the Story

- $4.5B in global AML penalties (2024).

- +417% surge in fines in H1 2025 alone: from $238.6M to $1.23B.

This isn’t overreach—it’s a recalibration. Adversaries upgraded their tools; regulators are forcing institutions to match.

What Changed (And Why It Matters)

Classic KYC assumed: verify document → verify person → move on. That worked when fraud meant physical forgeries. Today’s attackers bring:

- Synthetic identities that pass document checks.

- Deepfakes that mimic micro-expressions and liveness cues designed to catch analog deception.

Regulatory shifts:

- EU AMLR: risk scoring + beneficial ownership checks across the bloc.

- FinCEN: expanded Beneficial Ownership Rule (≈32M U.S. firms).

- FATF: explicit guidance on AI-manipulated identities—name-matching is insufficient.

- EU AI Act: machine-detectable/labeled AI content; penalties up to €35M or 7% of global turnover.

- U.S. 2025 policy signal: emphasis on innovation generated regulatory uncertainty in enforcement tempo.

- Singapore: mandates liveness + regular stress tests while supporting AI development.

One common thread: Static controls are finished.

The Enforcement Message

- Starling Bank: FCA fine £28.9M; 54k high-risk accounts opened despite restrictions.

- KuCoin: nearly $300M to U.S. authorities for enabling billions in suspicious flows.

- FCA 2024: £176M in fines (≈3× YoY).

- U.S. 2024: $4.3B+ in penalties.

Pattern: Programs acceptable five years ago now draw penalties that threaten franchise value.

The New Baseline

Perpetual KYC has replaced one-and-done.

What’s now table stakes:

- Continuous monitoring of identity and risk profiles.

- AI-powered detection across documents, voice, and facial biometrics in real time.

- Behavioral analytics (keystrokes, device fingerprints, geolocation patterns) moving from “advanced” to expected.

- Governance: NIST AI RMF, Basel oversight, model risk management.

- Incident readiness: rehearsed playbooks, simulations, and deepfake stress tests with evidence.

The sophistication gap is no longer banks vs. fraudsters—it’s prepared institutions vs. everyone else.

Where This Goes Next

- UK (Sept 1, 2025): Failure to prevent fraud offense—criminal liability for large orgs lacking reasonable prevention procedures.

- Global coordination: FSB, FATF, Basel aligning AI-risk standards.

- From pilots to policy: digital identity wallets, C2PA content authenticity moving toward compliance requirements.

Winners won’t “meet minimums”; they’ll treat AI-powered compliance as competitive advantage.

Building Defenses That Match the Threat

Generic checklists won’t cut it. You need verification-grade AI defenses that:

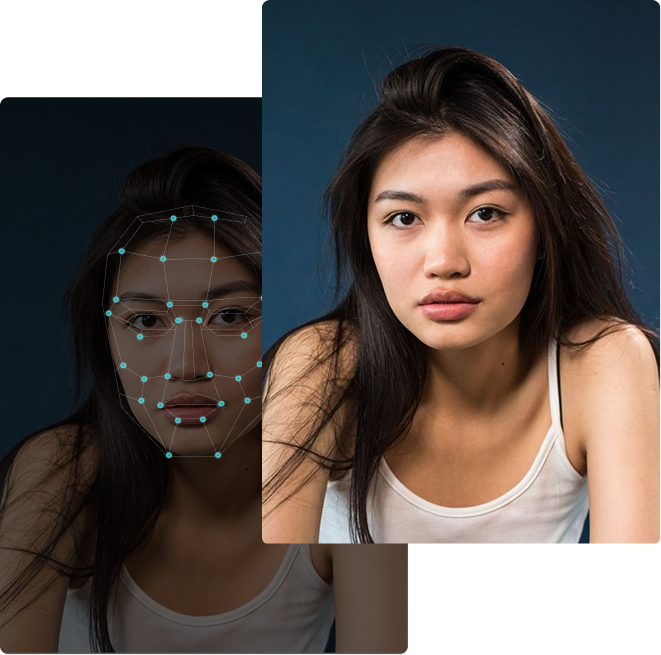

- Detect deepfakes across video, audio, and images at onboarding and re-authentication.

- Provide explainable outputs—which region, which anomaly, which manipulation, and how confident—so analysts and auditors can act.

- Deliver real-time liveness that separates a live person from high-fidelity synthetics.

- Slot into existing KYC/AML workflows without a re-architecture.

- Ship audit-ready evidence to satisfy EU AI Act / FinCEN / FCA / MAS expectations.

How DuckDuckGoose AI Closes the Compliance Gap

Built for regulated institutions that need results now:

Proven coverage

- 96% accuracy across image, video, and audio in production-like conditions.

- Real-time liveness and synthetic identity signals that standard KYC misses.

Explainability by design

- Per-signal evidence: regions, anomaly types, manipulation class, confidence.

- Analyst-ready views and audit-ready records for EU AI Act, FinCEN, and prudential reviews.

Operational fit

- Sub-second latency—no added friction for legitimate users.

- Seamless integration with your current KYC, AML, and fraud stacks.

- Adaptive modeling that learns from emerging attacker tradecraft.

Outcome

- Lower false positives, faster case handling, stronger regulatory posture—without sacrificing conversion.

The next billion-dollar fine is already in motion somewhere.

The question is whether it lands on an institution that waited—or one that adapted.

Contact us to assess your deepfake-detection readiness and benchmark your controls against 2025’s regulatory bar.

.webp)

About the author